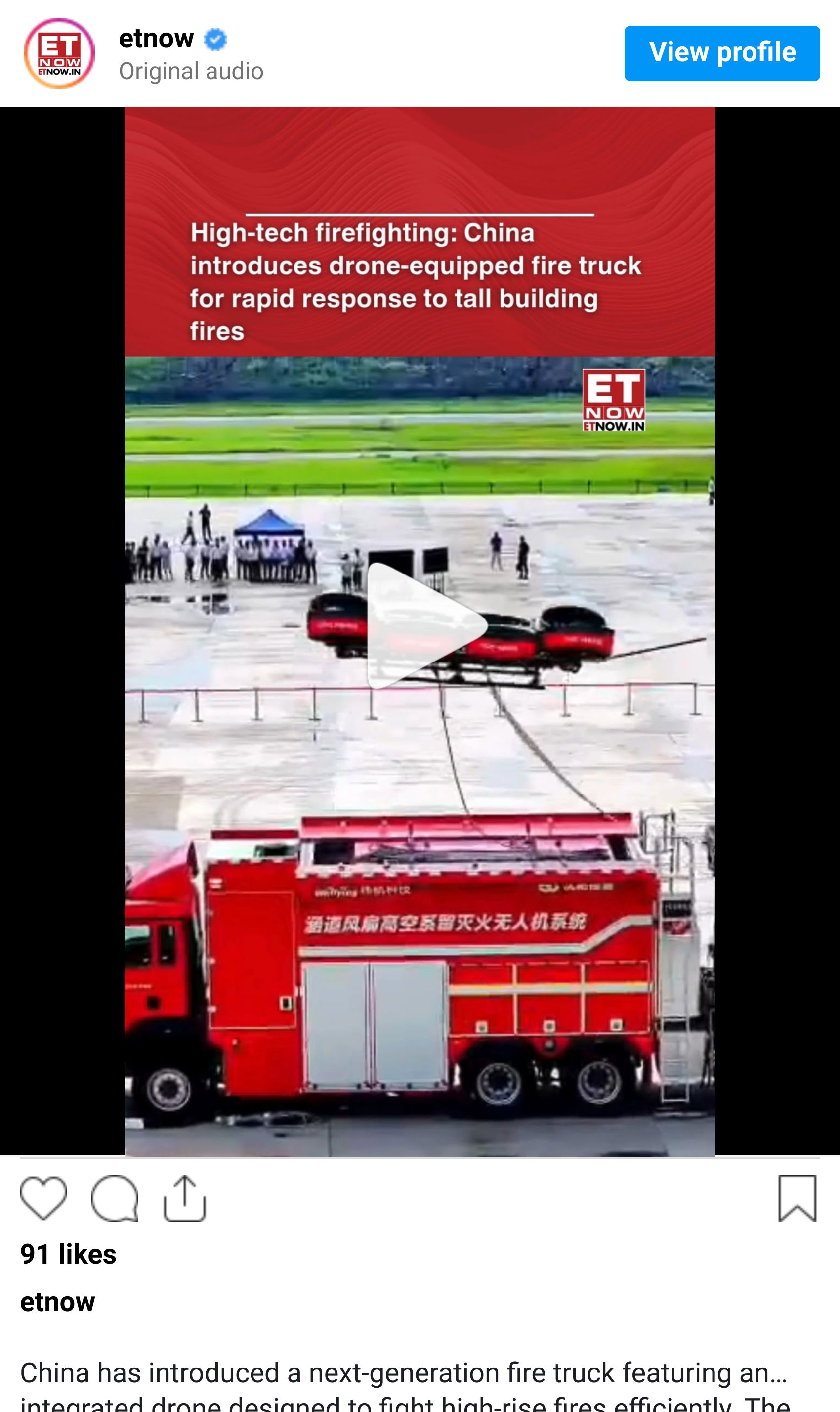

A few weeks ago I stumbled across a video that stopped me mid-scroll.

A fleet of red drones was swarming above a Chinese hillside, their coordinated movements looked like a robotic ballet. They were firefighting drones, part of a new fire truck that deploys autonomous aerial units capable of climbing 200 meters, spraying water 45 meters, and reaching places no traditional truck ever could. All deployed in under a minute.

As I was watching, I realized that this is what the first wave of mainstream robotics will actually look like.

For years, when people talked about robots, they usually meant humanoids like a C3PO from Star Wars. General-purpose machines that look roughly like us and, eventually, think roughly like us. Those robots will arrive one day, but they are not the first chapter of the story.

The first chapter is far more practical.

What we’re getting instead are specialized robots. Machines designed for narrow tasks where automation delivers immediate and obvious value.

Firefighting drones that can reach heights no ladder can.

Autonomous tractors that plant, spray or harvest with precision.

Inspection drones that patrol power lines, pipelines, and bridges.

Warehouse robots that move goods all day without fatigue.

None of these robots need to be charming. They don’t need to hold conversations or reason abstractly about the world. In many cases, they don’t even need the most advanced AI models.

They need to be reliable.

And reliability, in the physical world, starts with knowing exactly where you are.

Location, Location, Location!

I often focus on two things to measure progress in robotics:

Better intelligence (AI), which lets machines generalize across tasks and be more useful

Better hardware - the body, which expands what machines can physically do

But there’s one more dimension that’s missed by many, especially once robots leave the lab. I didn’t realise this too until I started looking into the research more deeply.

A robot doesn’t get to really “eyeball it.”

Most robots work in open, messy environments. Farms. Construction sites. Roads. Factories that look nothing like the CAD drawings. In those settings, small positioning errors turn into large outcomes.

If an autonomous tractor plants seeds a few meters off course, yields drop across an entire field. If a construction robot cuts in the wrong place, materials are wasted and schedules slip.

If a drone misjudges its position near infrastructure, it crashes.

Humans are good at absorbing uncertainty. We glance, adjust, and keep moving. Robots still struggle to do that reliably. When their sense of where they are drifts, performance collapses.

That gap is why one of the least exciting parts of the robotics stack ends up being one of the most important.

Location & Precision

If robots are going to operate autonomously at scale, they need to know exactly where they are in the real world, consistently. That is the problem GEODNET is focused on solving, using a decentralized network to deliver centimeter-level positioning to the machines.

The Problem With GPS (For Robots, Not Humans)

When people think about location technology, they think about GPS.

We trust GPS because, for most human use cases, it works well enough. It gets us from point A to point B. It helps us navigate unfamiliar cities (sometimes familiar ones too), and it powers everything from ride-hailing to food delivery. If I’m holding a phone to search for directions to the new Italian restaurant, being off by a few metres is fine. I look up and adjust myself.

Robots do not get that luxury.

GPS was designed for navigation, not control. Under the hood, it’s a probabilistic system. Signals leave satellites in orbit, travel tens of thousands of kilometers, pass through an electrically active atmosphere, bounce off buildings and terrain, and arrive with small delays and distortions.

It’s actually quite messy, because of physics.

For humans, that messiness is invisible. For machines, it is everything.

Most consumer-grade GPS systems drift by several meters, sometimes more, and the error isn’t consistent. It changes with weather, satellite geometry, and surroundings like trees or buildings. One moment you are two meters off, the next you are five. That variability is the real problem. Robots need repeatability, not just rough direction.

Engineers try to compensate by layering on sensors. Cameras, LiDAR, radar, inertial systems. These help, and modern robots use many of them together. But they add cost and complexity, and they often degrade in the same environments robots are sent into: dust, smoke, rain, fog, and low light.

Which is why, long before autonomous drones and tractors entered the spotlight, engineers working on precision systems looked for a different solution to location. One built for control.

A Precision Fix That’s Been Around for Decades..

None of this surprises surveyors or high-end agricultural operators. They’ve been dealing with the limits of GPS for decades, and solved it a long time ago.

The solution is Real Time Kinematics, or RTK.

The core idea is simple. Fixed reference stations are placed at precisely surveyed locations on the ground. Those stations receive the same satellite signals as nearby machines and experience the same atmospheric and timing errors. The difference is that the stations know exactly where they are supposed to be.

By comparing their known position with what the satellite signals report, the stations compute correction data and broadcast it in real time. Nearby receivers apply those corrections to their own measurements.

When that happens, GPS accuracy improves by orders of magnitude.

Meters become centimeters.

That jump is the difference between rough navigation and true control.

With RTK, machines can follow the same path day after day, return to the same spot reliably, and operate safely near boundaries, crops, or infrastructure. This is why RTK became standard in land surveying, precision agriculture, and construction long before autonomous robots entered the conversation.

So if RTK has worked since the 1990s, why is the world not already covered in centimeter-level positioning?

Because the problem was never the math. It was economics.

Why RTK Never Scaled

RTK worked well wherever they were deployed.

Surveyors used them to draw property lines. Construction crews used them to grade land. Large farms used them to guide tractors with repeatable precision. In those settings, RTK was effectively a solved problem.

What those systems were not designed for was scale.

Legacy RTK networks were built for a small number of professional users with fixed operating areas and a high willingness to pay. If you were a surveying firm or a commercial farm, paying thousands of dollars per year made sense. You only needed coverage where you worked, and the value was immediate.

How Traditional RTK Is Built

The dominant RTK providers, companies like Trimble, Leica Geosystems, and Topcon (see appendix), built networks the way industrial infrastructure has always been built.

Buy expensive, survey-grade GNSS receivers and antennas (~$10,000-$20,000+ devices)

Secure rooftops or towers with clear sky views through real-estate deals

Install and maintain power and internet connectivity

Monitor stations for uptime, drift, and failure

Each reference station is a small infrastructure project.

Even the largest legacy RTK networks today operate only on the order of a few thousand stations globally. In most cases, that means roughly 4,000 to 5,000 reference stations, heavily concentrated in high-demand regions like North America, Europe, and parts of Asia-Pacific. Coverage can be good within those regions, often spanning millions of acres, while large portions of the world remain sparsely covered or not covered at all.

And when I look into this more, it’s obvious that getting RTK to widespread use is hampered by an economic limitation, not a technical one. When each station is expensive to deploy and maintain, expansion naturally follows where there is predictable demand.

Dense cities, commercial farming regions, established industrial corridors.

Ubiquitous coverage was never the goal.

That tradeoff made sense when RTK served a narrow professional audience. It becomes a bottleneck once centimeter-level location is required by fleets of robots operating across diverse, dynamic, and unpredictable environments.

💡 Quick note:

GNSS stands for Global Navigation Satellite System. It is the umbrella term for all satellite based positioning systems, not just GPS.

GPS is the U.S. system, but there are others:

- GPS from the United States

- GLONASS from Russia

- Galileo from the European Union

- BeiDou from China

Why Tokens are a Natural Fit for RTK

Once you strip RTK down to its essentials, the bottleneck becomes clear.

RTK failed to spread because deploying and maintaining thousands of reference stations required centralized planning, upfront capital, and long payback periods.

Networks expanded where demand was already proven, not where future demand might emerge.

To me, that’s a coordination problem.

Let’s think about it from first-principles. RTK stations do not need to be owned by a single operator to be valuable. They just need to be accurate and stable.

The physical ingredients already exist in abundance. Rooftops. Power. Internet. Local operators who understand their environment. What was missing was a way to coordinate all of that without central ownership or long-term contracts.

This is an area where token incentives fit particularly well.

Instead of a single company deciding whether a location is worth covering, individuals make that decision themselves. The network rewards stations that add real value and reduces rewards when they do not. Coverage expands because it becomes locally rational to fill gaps, not because a central planner approved a budget.

Blockchains are good at exactly this kind of coordination. They let networks distribute incentives globally, adjust them based on real usage, and enforce performance rules transparently. Participants do not rely on promises. They can see how rewards are calculated and how quality is measured.

The result is a shift from planned coverage → emergent coverage.

Instead of building RTK networks one region at a time, the network grows wherever people are willing to deploy infrastructure. Over time, density increases in the places which was difficult to justify through traditional economics.

And this matters for robotics. I previously wrote:

…the macroeconomic case for humanoid robots is very strong. Human labor is by far the largest economic sector globally, at over $30 trillion annually. Labor shortages are rising due to lower birth rates, reduced immigration, and earlier retirements across major economies.

Labor is becoming more expensive and harder to find. This is a structural, not cyclical trend.

And that we’re likely to see rapid task expansion in the next few years. When robots are on the roads, in our homes, it's important that the infrastructure they will rely on exists.

GEODNET has been working to solve the coordination problem that kept precision location from becoming a default layer of the physical world.

Under the Hood: How GEODNET Is Actually Put Together

At a glance, GEODNET looks complex because it is solving several problems at once.

Collect raw satellite data from thousands of independent locations.

Verify that the data is real, accurate, and not spoofed.

Turn into positioning data machines can actually rely on

It also has to do all of that without owning towers or physical infrastructure.

The way GEODNET does this is by breaking the system into a few clear layers, each with a narrow responsibility.

The Edge Layer: Base Stations as Sensors, Not Infrastructure

At the edge of the network are GEODNET base stations - what the ecosystem calls “Satellite Miners.”

Each one has a deliberately narrow job. It listens to GNSS satellites, timestamps the signals precisely, and uploads raw observations upstream. Each station is low-power (<2W), uploads approximately 10-20 GB of mined data per month, and emits no radio frequency (RF) signals. And costs around $700.

That is it.

Almost no computation happens on the device itself. That’s a deliberate choice. It keeps the hardware cheap, power consumption low, and failure modes easy to detect.

GEODNET does not manufacture hardware directly. Instead, it certifies designs and partners with multiple GNSS hardware vendors globally. This creates a competitive hardware market where operators can buy compatible stations for a few hundred dollars rather than several thousand.

That immediately raises a reasonable question.

If legacy RTK vendors sold stations for $10,000 or more, how can a network built on much cheaper devices produce comparable precision?

The answer is that legacy RTK networks had to put accuracy into each individual station.

Those networks were sparse, often with reference points spaced 70-100 kilometers apart. When you only have a few stations covering a large area, each one must be extremely stable. That meant expensive survey-grade receivers, choke ring antennas to reject signal reflections, concrete pillars for stability, and professional installation.

GEODNET inverts that assumption.

The network pushes toward much higher density, often 20-30 kilometers between stations and sometimes closer. That means it no longer needs to depend on any single device being perfect. Modern multi-band GNSS chips, even inexpensive ones, observe the same satellite signals as legacy equipment. Individually they are noisier and more prone to drift. Collectively, they are powerful.

When dozens of nearby stations observe the same satellites through the same atmosphere, the network can cross-check them. Stations that drift relative to their peers stand out. Multipath errors become statistical noise. Faulty or spoofed data becomes detectable because it breaks correlation patterns. GEODNET trusts stations because they behave consistently over time relative to their neighbors.

This is the same transition computing went through decades ago. Early mainframes assumed machines could not fail and spent heavily to prevent it. Distributed systems assume failure is normal and design around it. GEODNET applies that mindset to positioning.

There is another subtle point I want to make. Because stations upload raw observations rather than computed positions, the most sensitive math happens centrally. That allows the network to improve correction models over time, adjust weighting dynamically, and apply new algorithms. The station is a sensor, but the real intelligence lives elsewhere.

So:

Cheaper hardware makes density economically viable.

Density makes network-level validation possible.

And network-level validation is what allows centimeter-level positioning without centralized ownership.

Once you see that structure, GEODNET stops looking like a cheaper RTK vendor and starts looking like a distributed sensing network.

Geography as Architecture

But density alone isn't enough. It needs to be the right kind of density.

RTK corrections are inherently local. A base station only helps machines within a few tens of kilometers because atmospheric errors decorrelate with distance. A thousand stations clustered in California do nothing for a farmer in Iowa.

It’s the same problem that all crowd-source infrastructure protocols face, including Helium (mobile networks) and Hivemapper (mapping the globe using car devices). People deploy where it feels safe and familiar, and vast areas stay empty. GEODNET needed a way to spread coverage intelligently without centrally planning every deployment.

So…how about turning geography into a first class architectural constraint?

The Earth's surface is divided into hexagonal cells, each representing a local coverage zone. Hexes are a practical way to ensure roughly equal distances between stations and avoid the distortions you get with square grids. This gives the network a precise way to reason about coverage: instead of saying "Europe is well covered," GEODNET can see exactly which hexes are dense, sparse, or empty.

Then incentives do the steering. The first station in a hex to maintain high-quality data (98%+ uptime for 30 days) earns a Location NFT, and that NFT holder receives full rewards regardless of how crowded the hex gets later. Everyone else who comes in later split a separate reward pool among themselves.

So if you're eyeing a hex that already has an NFT holder and a few other stations, your potential earnings are a fraction of what you'd get by finding an empty hex and claiming it first. Operators spread out naturally because the math rewards pioneering over piling in.

The effect is a strong first-mover advantage. Get to an empty hex early, install carefully, maintain performance, and you've locked in your position. Latecomers face diluted economics.

Who actually deploys these stations? The majority are individuals and hobbyists, not professional infrastructure operators. About one-third of the network's base stations are run by operators with 10 or more miners, suggesting a mix of casual participants and more committed deployers who've scaled up after seeing the model work.

Source: GEODNET Console

Verification: Proving the Data Is Real

Decentralized networks are supposed to be “trustless”, which means trust is implied and not assumed. So… it only works if the network can tell good data from bad data, whether the problem is noise, misconfiguration, or intentional manipulation.

Verification is the magic ingredient.

GEODNET does this through proof of location and proof of accuracy.

Every certified station has a cryptographic chip that creates a hardware-bound identity. Data is signed at the device level, which prevents basic spoofing or replay attacks. The team has actively detected attempts to fake stations, using both the crypto chip verification and GNSS analysis tools to identify anomalous data patterns.

More importantly, stations are constantly evaluated against nearby stations that are observing the same satellites through the same atmosphere. In a local area, those observations should correlate tightly. When a station drifts, suffers from interference, goes offline intermittently, or reports measurements that diverge from its peers, it stands out statistically.

The response is automatic. Rewards adjust downward as quality degrades. Stations that remain inconsistent lose influence over time and eventually become economically irrelevant.

There’s no need for manual policing or a trusted central operator to make decisions. Performance determines influence.

This is why cheaper hardware does not degrade the network. GEODNET does not assume stations are perfect. It assumes they are observable, comparable, and replaceable. Accuracy emerges from agreement over time.

The Processing Layer: Turning Raw Signals into RTK

Raw GNSS observations are not useful on their own. They become valuable only after they’re processed, validated, and combined.

GEODNET does this in the cloud.

Stations stream raw observations into backend systems where data from many nearby stations is aggregated. Low-quality inputs are downweighted or excluded. The remaining data is fused to generate real-time correction streams using standard RTK delivery methods such as NTRIP.

From the rover’s point of view, nothing here looks exotic. The receiver connects to a correction service and receives a virtual reference stream synthesized from nearby stations. Except that the network behind it is 4x denser than most RTK alternatives. The result is 1–2 centimeter horizontal accuracy, as good as equipment that costs 10–20x more.

Let me be clear that GEODNET is not trying to invent new positioning standards! It uses the same GNSS signals, the same RTK math, and the same client interfaces that robots and machines already support. The innovation is in how the data is sourced, verified, and made economically viable at scale.

This is also where the blockchain fits, and where it does not. The blockchain governs identity, incentives, and validation logic. It decides who gets paid and why. The positioning engine itself runs on conventional cloud infrastructure.

Seen end-to-end, GEODNET’s architecture makes a very specific bet:

Precision positioning doesn’t require perfect stations.

It requires dense, honest measurements and a system that knows how to ignore bad ones.

That bet allows GEODNET to use cheaper hardware, scale faster than centralized networks, and push RTK into places it was never economical to reach before.

Demand: Is Anyone Actually Paying for This?

Architecture is easy to admire. Revenue is harder to fake.

Crypto has produced no shortage of beautifully designed networks with clever incentives, impressive node counts, and essentially no real customers. That history makes the obvious question unavoidable: is GEODNET building infrastructure that people actually pay for, or infrastructure that hopes demand shows up later?

On this front, the data is unusually clear. GEODNET already has real demand, and it is growing fast enough to matter.

In Q3 2025, GEODNET generated over $1.2M in revenue, up 28% from the previous quarter and up 217% year-over-year.

In Q4 2025, that number increased to $1.76M in revenue, continuing its consistent growth trajectory.

In the first 2 months of 2026 alone, ~$1.25M in revenue. That puts annualized revenue run-rate at ~$7.5M, making it one of the top-earning DePIN protocols in existence.

According to Messari's State of DePIN report, only 25 out of 80 analyzed DePIN projects generate any revenue at all. The median revenue for Physical Resource Networks is around $730,000.

GEODNET is operating at multiples of that level.

And what strikes me is that the revenue is not cyclical like most crypto revenue (which depends heavily on speculation or transaction fees). The revenue is coming from enterprise customers with real-world use cases: Propeller (construction site mapping), DroneDeploy (aerial surveying), Quectel (IoT chipsets), the USDA (precision agriculture outreach), and dozens of others.

The network now spans ~21,000 active Satellite Miners across 5,000+ cities in 150+ countries.

That coverage is what makes the product work.

The GNSS correction service market sits at roughly $3.4 billion today and is projected to hit $6 billion by 2030. Here's where GEODNET fits across the key segments:

Most Promising: Drones & Robotics

Every DJI Enterprise drone supports RTK. Thousands fly on GEODNET's network daily. Propeller (construction monitoring) and DroneDeploy (aerial surveying) have announced formal integrations.

And on the industrial AgriTech end, GEODNET has also partnered with DroneDash (via GeoDash Aerosystems) to build a heavy-lift agricultural UAV that pairs centimeter-level RTK positioning with onboard AI vision, the kind of “spray/spread/haul” platform where precision directly translates into less waste and lower cost per hectare.

Drones and AgriTech represent GEODNET's largest customer segments today, with drones and robotics scaling surprisingly fast over the past year. Ten million drones ship annually, and the high-end ones need centimeter accuracy. Same with newer specialized robots like robotic lawnmowers, inspection bots, and autonomous agricultural machines.

Boson Motors demoed an autonomous electric truck running entirely on GEODNET. This segment is hard to size precisely, but it's growing fast and plays to GEODNET's cost advantage: legacy RTK pricing doesn't work for a $400 lawnmower or $1,500 drone.

GEODNET is also starting to show up in more consumer-facing drones, not just enterprise drone fleets. Recently, it teamed up with HYFIX Spatial Intelligence on GEO-SWARM, an autonomous “drone-in-a-box” home security system, framed as safe deterrence + aerial situational awareness, with the first release targeted for Q4 2026.

Steady traction: Agriculture

Agriculture is a more mature market, but still strategically important. Precision agriculture has used RTK for years to enable auto-steer tractors, optimized planting, and reduced input waste. The bottleneck has always been coverage and cost, especially in rural areas. Traditional subscription models were expensive and often failed to reach the fields that needed them most.

This is where a decentralized network has a natural edge. One North American dealer alone installed 200 GEODNET stations in a single season. The USDA (US Department of Agriculture) has validated the service and is actively onboarding smaller farmers. All three major tractor manufacturers sell compatible equipment. By 2030, agriculture is expected to represent roughly 30 percent of the correction services market, and rural coverage is exactly where centralized networks struggle.

Tough market: Surveying & Construction

This is on the other end of the spectrum. It demands sub-centimeter accuracy and carry real liability risk. Trimble and Hexagon dominate with integrated hardware-software stacks and decades of relationships. GEODNET can play at the edges, but I don’t think this is where it wins first.

Promising with caveat: Automotive ADAS (Automotive Advanced Driver Assistance Systems)

Lane-keeping systems for autonomous vehicles need better than 3–5 meter GPS accuracy. GEODNET has a partnership with ByNav, a Tier 2 automotive supplier building ADAS modules.

The volumes are still ramping, but the unit economics are attractive: millions of cars, each needing continuous corrections. This segment (expected to be ~20% of the high-precision positioning market by 2030) demands extreme reliability and SLAs in order to win the deal. GEODNET is building toward it, but incumbents still have the advantage here.

ROVR: Mapping the Roads Robots Will Drive On

There's a parallel infrastructure problem hiding behind autonomous vehicles: maps.

Self-driving cars need centimeter-accurate 3D maps of the roads they're traveling with lane markings, curb heights, sign positions, etc. Today, this data comes from expensive survey vehicles operated by a handful of companies, creating proprietary datasets that cost automakers millions to license.

ROVR Network is trying to decentralize that. And GEODNET is betting on them.

In April 2025, GEODNET co-led ROVR's $2.6 million seed round alongside Borderless Capital. The investment was their effort at vertical integration.

ROVR's hardware relies on GEODNET's RTK corrections to achieve centimeter-level accuracy. When a ROVR contributor drives with a ROVR mapping device in their car, it connects to GEODNET's network to transform rough GPS into precise coordinates. That precision is what makes the resulting 3D data valuable to automakers.

The integration goes deeper than technology. ROVR's tokenomics include a burn mechanism where 20% of all data sales revenue buys back and permanently burns GEOD tokens.

Every time an automaker purchases mapping data from ROVR, value flows directly back to GEODNET's token economy. The two teams have even co-located their Silicon Valley offices.

This is GEODNET playing the long game, by investing in applications that create structural demand for its infrastructure, capturing a slice of every transaction through the burn mechanism. If ROVR succeeds, GEODNET becomes an embedded, non-optional layer in the autonomous vehicle stack.

And if autonomous vehicles become the dominant transportation paradigm over the next decade, GEODNET has effectively bought a second ticket to that future, one where it wins whether customers come directly or through the mapping layer that depends on it.

The Demand Curve That Hasn't Arrived Yet

Honest picture of where GEODNET sits today?

Most of the current revenue comes from sectors where RTK has existed for years like precision agriculture, surveying, drone mapping, construction.

These are customers that Trimble, Hexagon, and other legacy players have served for decades. GEODNET wins some of this business on price and coverage, but it's competing on established turf. The incumbents know these customers. They have the relationships, the certifications, the enterprise sales teams.

That's fine for now. It pays the bills. It funds the burns. It proves the network works. But it's not the endgame.

The real opportunity is the wave yet to hit - the mass deployment of autonomous machines at price points where legacy RTK economics simply don't work.

Think about it this way: a $200,000 tractor can absorb a $1,000/year RTK subscription. A $1,000 robotic lawnmower cannot. A $400 delivery robot definitely cannot. As the cost of robots keeps dropping and ship in higher volumes, the addressable market for positioning services expands dramatically, but only for providers that can serve those price points profitably.

GEODNET is using today’s revenue to prepare for that moment. The network is densifying. Reliability is improving. Relationships with robotics teams are forming before mass deployment. These partnerships do not drive material revenue yet, but they position GEODNET as the default positioning layer when those products scale.

Elon Musk talks about humanoid robots in every home within a decade. On our end, we believe usable, reasonably priced humanoids will happen within 5 - 10 years. We laid this out in our machine economy thesis, explaining how the path forward will unfold in 3 phases, culminating in rapid task expansion from 2028 onwards:

As capability jumps, cost drops. Wright’s Law kicks in: every doubling of production drops unit cost on a predictable curve (~20%). It happened with solar, it happened with semis, and it will absolutely happen here.

Unlike autonomous driving (which took a decade of incremental progress), robotic manipulation will scale faster because mistakes are often recoverable and environments are more structured.

So the clock is ticking. By the time the robotics wave arrives in force, the real question is whether GEODNET will have the coverage, the uptime track record, and the unit economics to capture it.

Compared to a year ago, the answer increasingly looks like yes.

Business Model: How GEODNET makes money

GEODNET is best understood as a data business with a capital-light infrastructure model.

It sells data subscriptions. Enterprises pay subscriptions for access to real-time GNSS correction streams, billed monthly or annually, much like a SaaS product. A drone operator, robotics company, or agriculture platform signs a contract, receives credentials, and their machines begin pulling centimeter-accurate positioning data in production.

The pricing undercuts incumbents significantly because GEODNET doesn't carry the cost structure of owning 21,000 base stations.

The physical infrastructure is deployed by independent operators, on their own rooftops, using their own capital. GEODNET coordinates the network, validates data quality, and sells the resulting service.

This dramatically reduces the capital required to scale revenue by pushing capex and opex costs to the operators.

But the system only works because the operators are incentivized to expand coverage and maintain uptime. That’s where the token comes in.

The GEOD token is the mechanism that bootstraps supply before demand fully materializes and then captures value as usage grows. Understanding how supply flows out and demand flows back in is the key to evaluating whether the model is sustainable.

Supply: What Goes Out

Total supply is capped at 1 billion GEOD. No more will ever be minted.

The initial allocation:

Source: GEODNET Docs

Mining: 35% (flows to base station operators over time)

Team: 25% (multi-year vesting)

Investors: 25% (multi-year vesting)

Ecosystem: 10% (grants, partnerships, development)

Public sale & marketing: 5% (initial liquidity and go-to-market)

Mining rewards follow a Bitcoin-style halving schedule, compressed to annual cycles. Before July 2024, a station earned 48 GEOD daily. Now: 12 GEOD (~$1/day and varies based on token price). By 2027: just 6 GEOD daily.

This creates urgency. Early deployers capture rich rewards. Later entrants earn fewer tokens but (theoretically) at higher prices as the network matures and the price per token increases. The emission curve is designed to bootstrap aggressively, then taper as organic economics take over.

Two additional mechanisms shape how supply gets distributed.

First, rewards are now performance-based, meaning stations with poor uptime or noisy data see rewards reduced, pushing quality up without increasing emissions.

Second, SuperHexes let the community stake tokens to boost rewards in underserved areas recognized by GEODNET, steering coverage toward high-value regions rather than letting it cluster randomly.

As of February 2026, about 62% of the total supply has unlocked. Daily emissions from ~21,000 active miners range from 200,000 to 300,000 GEOD.

Demand: What Comes Back

Here's where GEODNET diverges from most crypto projects. There are multiple mechanisms that create structural demand for GEOD with actual utility that requires holding or spending tokens.

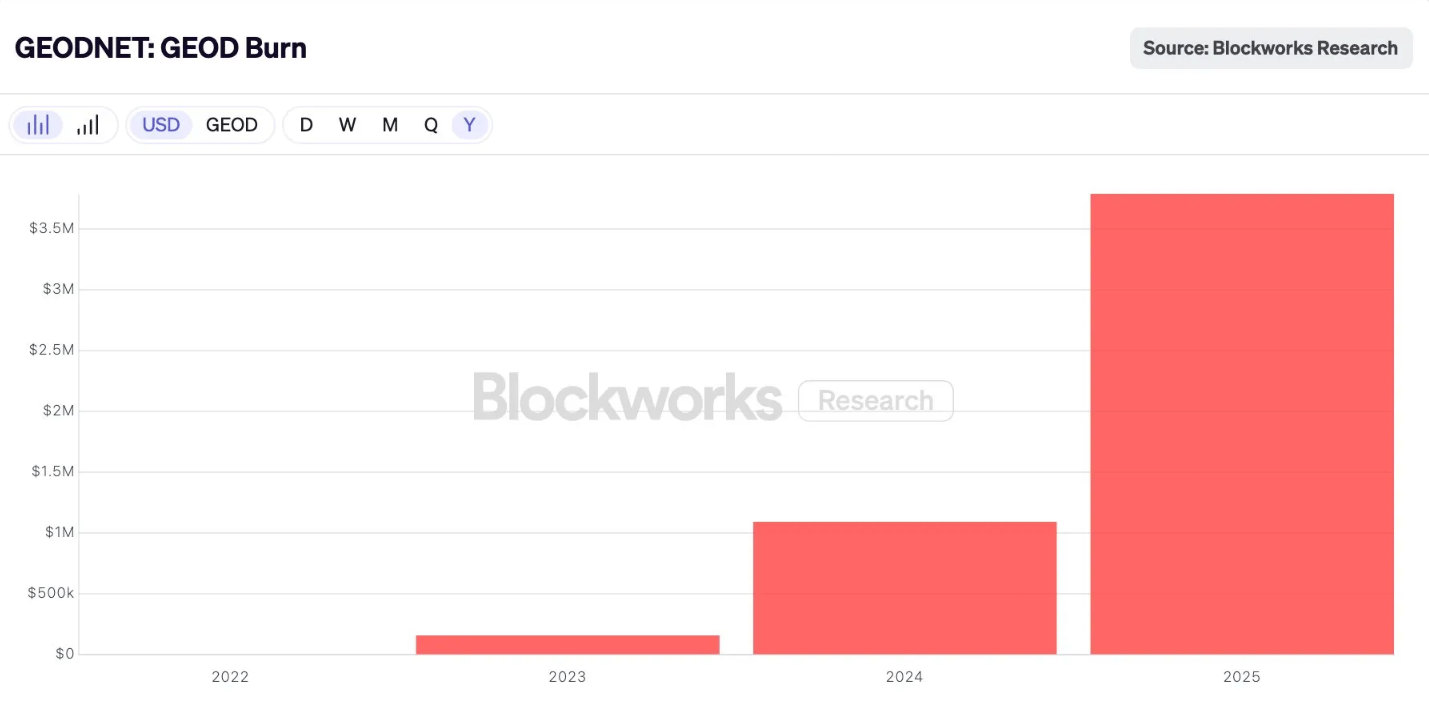

The Burn: Revenue-Driven Deflation

The primary mechanism. When customers pay for RTK data (mostly in fiat), through enterprise contracts, 80% of that revenue buys GEOD on the open market and permanently destroys it. The remaining 20% funds GEODNET Foundation operations.

This has been live since day one, executed programmatically and visible on-chain:

2023: ~$100K burned

2024: ~$1.1M burned

2025: ~$3.5M+ burned

Source: Blockworks

Over 1 million GEOD burned in a single recent week.

More customers using data → more revenue → more tokens permanently removed from supply.

2. SuperHex Staking: Locking Tokens to Steer Coverage

The SuperHex program lets anyone stake GEOD to activate high-priority coverage areas. Want to incentivize deployment in rural Vietnam or agricultural Argentina? Stake 20,000 GEOD to make that region a SuperHex, and miners who deploy there earn up to 4x normal rewards for a year.

Stakers earn a 20% bonus when their tokens unlock after the one-year period but during that time, those tokens are completely out of circulation. This creates meaningful lockup: as of recent data, over 7.4 million GEOD was staked across active SuperHexes. That's demand driven by network utility, not trading.

3. Governance: Voting Rights Require Skin in the Game

GEODNET runs an on-chain governance system. To vote on proposals, you need voting power. That comes from three sources: holding a Location NFT (earned by being first to produce quality data in a hex), staking GEOD in SuperHexes, or holding locked tokens.

Participants who want influence over the protocol's direction need to hold or stake GEOD to get it.

The combined effect is meaningful.

Between burns, SuperHex staking and governance participation, there's constant structural pressure removing tokens from liquid circulation. Not all demand drivers are equal but together they create a thicker floor under the token than pure speculation would provide.

How It All Connects

Now you can see the full loop.

Emissions pay station operators to deploy and maintain infrastructure. That is the upfront cost of building the network. GEODNET is spending tokens to buy coverage, before demand fully matures.

Revenue flows in when customers pay for the data that infrastructure produces. That is real-world value entering the system

Burns remove tokens from circulation proportional to revenue.

The critical question for any crypto protocol: when does burn exceed emissions?

Let's do the math. Current daily emissions are roughly 275,000 GEOD (a rough estimate across ~21,000 miners at varying reward tiers). To offset that entirely through burns at $0.16/token, you'd need about $44,000 in daily revenue, roughly $16 million annually.

GEODNET is not there yet. Based on the Q4 2025 run rate, annualized revenue is approaching $7 million. At that level, burns offset roughly 35-40% of emissions. The system remains inflationary, but the gap is materially smaller than it was a year ago.

If the 200% year-over-year growth is maintained, deflationary crossover becomes plausible within 12–18 months. That outcome is not guaranteed. Growth can slow. Token prices change the math. But it’s within striking distance.

What This Actually Means

Most tokenomics are faith-based. You believe emissions will attract supply, and you hope demand materializes later. The token trades on narrative in the meantime.

GEODNET is further along that curve. The demand side is already generating millions in revenue. The burn isn't theoretical - you can literally watch it happen weekly on Dune. The link between machines consuming RTK data and tokens leaving circulation is direct and mechanical.

CEO Mike Horton has compared this dynamic to Apple’s long-term share buybacks, which cut its share count by nearly 50% over two decades. Short-term, the buybacks barely registered against broader market forces. Over decades, the reduction in share count compounded quietly and meaningfully.

GEODNET is running the same playbook, just transparently and on-chain. The burns are not designed to pump the token price in the short term. They are designed to make the long-term math work, balancing the cost of early bootstrapping with durable value capture as the network scales.

2024-2025 proved the mechanism functions. 2026 is all about getting to the inflection point from inflationary to deflationary.

The burn chart will tell the story.

The Founder Who Had Already Seen This Movie Before

This idea that RTK didn’t need better technology so much as a better coordination model wasn’t obvious to most of the precision-GPS industry.

But it was familiar to Mike Horton.

Horton’s career has a consistent pattern: he shows up early to a technical shift, gets told the cheaper approach won’t work, and then builds it anyway.

Mike Horton

In the mid-1990s, fresh out of Berkeley with a master’s degree in electrical engineering, Horton co-founded Crossbow Technology. At the time, he was experimenting with MEMS sensors, which are tiny accelerometers and gyroscopes etched onto silicon chips. Aircraft navigation systems relied on mechanical gyroscopes the size of softballs, spinning at thousands of RPMs. They were expensive, fragile, and prone to failure.

Horton’s claim was simple and heretical: you could replace them with chips smaller than a fingernail.

The industry response was predictable. MEMS sensors were cheaper, which meant they were assumed to be worse. They were noisier. They drifted more. They didn’t have decades of flight history behind them.

Horton built Crossbow anyway.

Over time, Crossbow’s MEMS-based navigation systems proved reliable enough to earn FAA approval. In 2003, MIT Technology Review named Horton one of the top innovators under 35. In 2011, Crossbow was acquired by Moog Inc for a reported fee of $32 million. It was a successful exit, but more importantly, it cemented a lesson Horton would carry forward: when incumbents say something is “too cheap to work,” they’re often describing their business model, not the limits of physics.

After Crossbow, Horton went deeper into GPS and GNSS. As autonomous systems started to move from theory to reality, he became fixated on precision systems. He could see the future clearly enough: drones, agricultural automation, autonomous vehicles. None of it would work at scale without centimeter-level positioning.

So he did what experienced founders do. He tried to build it.

The Turn

By the late 2010s, Mike Horton already knew the conclusion.

RTK worked. Centralized deployment didn’t.

After years inside precision navigation, the technical path forward was clear, but the organizational one wasn’t. The economics of traditional RTK networks simply didn’t match the scale an autonomous future would require.

Then, in 2019, Horton noticed something happening outside his industry.

Helium launched with a counterintuitive idea: instead of building a wireless network itself, it let individuals buy inexpensive hardware and deploy it where they lived. Coverage scaled not because a company planned it, but because participation made local sense.

The parallel was immediate.

RTK, like wireless networks, depends on dense geographic coverage. RTK base stations, like hotspots, can be relatively simple devices. And RTK corrections, like data, are locally relevant as you only need them from nearby nodes.

There was one detail that made the comparison even more compelling: RTK base stations could be cheaper than cellular hotspots. They didn’t need to transmit signals or handle complex processing. They just needed to receive satellite data and upload it.

That was enough to flip the problem.

What if RTK didn’t need to be built by a company at all? What if it could be built by its users, coordinated through incentives?

With that insight, Horton co-founded GEODNET in 2021.

Team and Fundraising

Mike Horton didn’t build it alone, he had assistance from some of the leading industry experts and innovators:

Yudan Yi (Co-founder & GNSS Lead) spent 10 years at Topcon, 2 years at Qianxun SI (China's largest RTK provider), and 3 years at Aceinna. PhD in Geodesy from Ohio State. He’s built RTK networks from the inside at the incumbents GEODNET is now competing against.

David Chen (Blockchain Lead) brings 20+ years of technical leadership in Silicon Valley, in crypto since 2013, and co-founded blockchain projects Jingtong and MOAC. The token model only works if the on-chain infrastructure is solid, and that's his job.

Domain expertise plus crypto infrastructure experience. The perfect founder team fit to solve this problem.

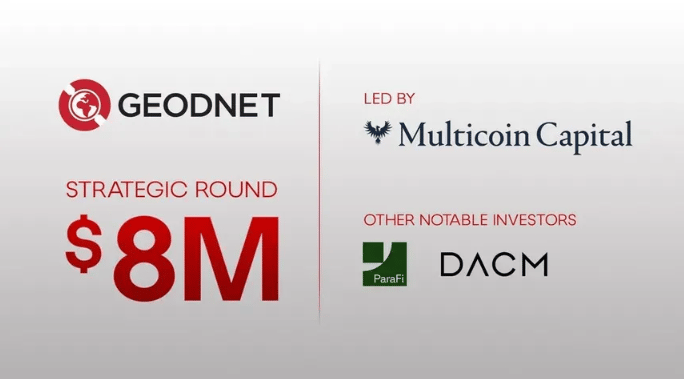

With regards to fundraising, GEODNET has raised $15 million across six rounds since 2023, with a cap table that's gotten progressively stronger:

Private Token Sale (July 2023): $1.5M — Borderless Capital, IoTeX

Seed Round (February 2024): $3.5M — North Island Ventures, Borderless, IoTeX, Road Capital, Modular Capital, Reverie, JDI, Tangent

Strategic Round (April 2024- December 2024): $2M — Pantera Capital, CoinFund, VanEck, Santiago R. Santos, Animoca Brands, ParaFi Capital

Strategic Round (February 2025): $8M from Multicoin Capital, ParaFi Capital, DACM

$15 million still isn't a massive war chest by crypto standards but GEODNET's model doesn't require one. The capital-intensive part (deploying 20,000 stations) was funded by token emissions to distributed operators, not equity dollars to a centralized buildout. The fundraising covers protocol development, BD, and Foundation operations while the network funds itself.

Our Thoughts:

The Real Moat Is Time

The DePIN playbook is public. The RTK algorithms are well-understood. Multi-band GNSS chips are a commodity. So what stops someone from copying this?

More than you'd think.

Each GEODNET base station contains a cryptographic chip that locks the hardware to the GEODNET network. Stations cannot dual-mine or be repurposed for a competing network. A competitor couldn't simply launch “better software” and convince existing operators to switch, they'd need to convince them to buy entirely new hardware.

But the deeper moat is the two-sided network and the capital required to break it.

GEODNET has 21,000+ stations deployed across 150 countries. More importantly, it has customers paying for the data those stations produce. Real enterprises with integrated workflows. That revenue funds the burn that makes operator economics work.

A competitor trying to poach operators faces an ugly math problem. To attract operators, they would need to offer higher rewards than GEODNET. But without customers, those rewards are pure subsidy. To attract customers, they would need comparable coverage and reliability, which requires operators first. Bridging that gap means burning capital on both sides of the market at the same time.

That's not impossible. A large firm with deep pockets could theoretically subsidize both sides long enough to compete. But the capital required is high and the payoff timeline is long. “Theoretically possible” does not mean economically attractive.

Meanwhile, GEODNET's network effects compound.

More stations → better coverage → more customers → more revenue → better operator economics → more stations.

Each cycle makes the replication cost higher. The bootstrapping window that GEODNET used is closing because the economic moat gets wider every quarter.

The moat isn't the technology. It's not even the hardware. It's being three years ahead on a two-sided network where both sides reinforce each other and where catching up requires burning capital against an incumbent that's already generating cash.

Challenges Ahead

GEODNET has to run an extremely reliable global real-time service business. That is hard, but it is also where a lot of defensibility can accumulate if they do it well.

Token volatility is the other obvious risk. If GEOD prices are depressed in a severe bear market, the incentives may not be enough to entice operators. The mitigation is that revenue/burns will continue to support token price and give it a floor. That said, this remains a meaningful sensitivity.

A few things I’ll be watching for:

Revenue concentration, to understand how diversified demand really is.

Revenue durability across crypto market cycles to see if usage persists

Churn and contract duration to gauge how sticky GEODNET’s enterprise relationships actually are.

Those indicators will say far more about the business's health than the token's price in any given month.

The Boring Layer That Makes the Exciting Stuff Work

Go back to the firefighting drones swarming a hillside in China.

They did not need artificial general intelligence. They did not need to understand fire. They needed to know exactly where they were, relative to each other and the terrain, with enough precision to move fast without crashing.

That's the unsexy reality of the robotics revolution. The exciting part is the swarm, the autonomy, the AI. The essential part is the positioning layer underneath, the infrastructure that tells every machine where it is, centimeter by centimeter, second by second.

For decades, that layer was too expensive to scale. RTK worked, but the economics didn't. Building global coverage required centralized capital, centralized planning, and centralized risk, which meant it grew slowly and served only those who could pay premium prices.

GEODNET cracked that problem by making it someone else's problem, twenty thousand someone else’s, each deploying a station because the math made sense for them individually. And crypto made the coordination work.

The result is a network with unmatched coverage, real revenue from real enterprises, and a model where increased usage translates mechanically into value capture.

Is it a sure thing? No. The robotics wave could take longer than expected. Incumbents could adapt. Execution risk is real.

But if the thesis is right, that the next decade brings millions of machines that need to know precisely where they are, then someone has to build the positioning layer they'll run on.

GEODNET is already building it.

The robots are coming. They're going to need directions.

Thanks for reading,

Teng Yan

Useful Links:

Disclosure: This essay was supported by GEODNET, which funded the research and writing.

Chain of Thought kept full editorial control. The sponsor was permitted to review the draft only for factual accuracy and confidential information. All insights and analysis reflect Chain of Thought’s independent views. Where tradeoffs or limitations exist, they are stated clearly.